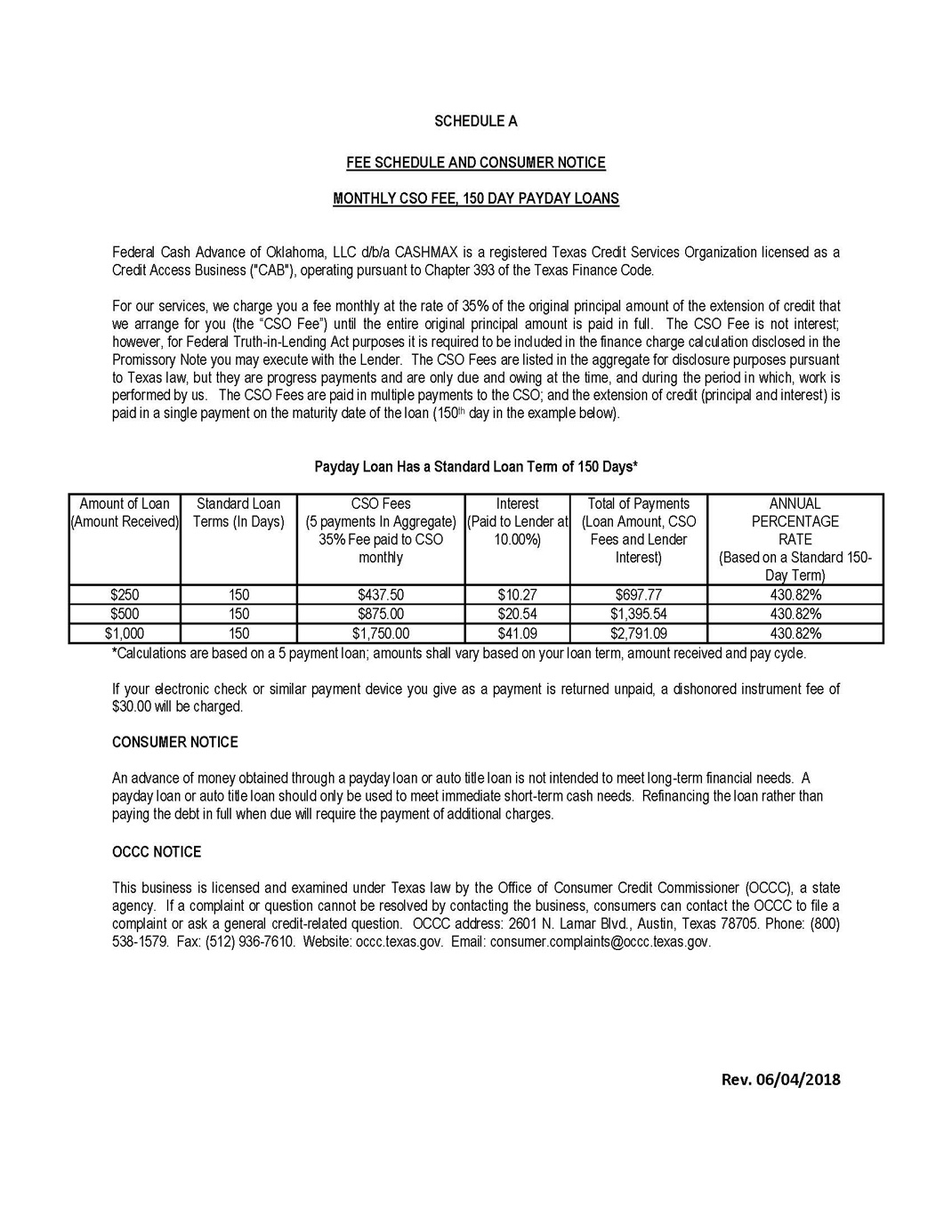

To make sure a delicate underwriting procedure, we will display rewarding tips and you can understanding so you can sail using so it critical stage on your own road to homeownership.

Very, let’s plunge for the arena of financial underwriting, and help your perfect from home ownership take the last methods towards the facts.

What’s Financial Underwriting?

Mortgage underwriting is the procedure which a lender determines if or not a debtor is eligible to have an interest rate. This new underwriter often feedback this new borrower’s credit rating, earnings, expense, and you will assets to assess the possibility of financing currency into the borrower.

The underwriting techniques generally starts with the fresh debtor submitting a loan app. The application form will include factual statements about the fresh borrower’s income, debts, assets, and you may credit score. The lender will also purchase a credit report and you will an assessment of the house your borrower is seeking buying.

The newest underwriter have a tendency to remark the latest borrower’s app and you will supporting papers, It is to select the borrower’s personal debt-to-income proportion, credit score, or installment loans no bank account Alberta other issues affecting the possibility of financing currency so you can brand new debtor. The new underwriter may also think about the worth of the property one to new borrower wants purchasing plus the amount of the new loan that the borrower are requesting.

In line with the guidance achieved from inside the underwriting processes, the new underwriter will make a decision regarding the whether or not to agree or refuse the mortgage app. If for example the loan is approved, the lending company commonly topic a connection page into the debtor. The newest union page tend to description this new terms of the mortgage, for instance the interest rate, amount borrowed, and cost several months.

How much does a keen Underwriter Would?

Mortgage underwriters have the effect of determining loan applications to determine approval. It works for a loan provider and evaluate the borrower’s financial situation and you will amount of chance. Underwriters get acquainted with money, possessions, credit rating, and family appraisal making acceptance choices, to try out a crucial role regarding home mortgage process .

They interact with Loan Officers to get expected files and guidance getting determining the fresh borrower’s chance peak. On top of that, Mortgage Officers help in ensuring all of the necessary papers is actually registered getting a silky techniques.

- Determining brand new Home’s Value: An appraisal can be used to find the value of your house we want to buy in comparison to the seller’s price tag, making certain you’re not investing more the home was really worth . New underwriter feedback the assessment to confirm the residence’s real really worth aligns for the amount borrowed, reducing the lender’s risk and securing the buyer out of overpaying.

- Researching Your credit report: Loan providers have confidence in your credit history to assess the qualification and you may approval for a financial loan. They consider not merely your credit score, also your existing discover accounts, late payments, bankruptcies, and borrowing from the bank utilization to evaluate debt designs and you will reputation of financial obligation payment.

- Verifying Income & Employment: Lenders want to select a stable a job reputation for no less than 2 yrs in the same reputation otherwise field just before granting an effective financial. It reveals a reliable income source to support their month-to-month home loan repayments . On the other hand, it find out if their said money for the application aligns that have your own real income to make sure mortgage payment function.

- Examining Down-payment & Savings: In advance of mortgage recognition, the brand new underwriter inspections which you have adequate money into the property’s downpayment and you can recommendations your own offers to cover more costs such as for example closing costs . Specific finance, such as for instance Virtual assistant financing to own eligible pros and you may productive-obligations provider members, will most likely not wanted a down payment, in which case the underwriter doesn’t be certain that this type of needs.

Sooner, underwriters dictate mortgage acceptance, so it is crucial that you support the procedure by providing punctual and you can a record immediately following and come up with an offer towards the a house .